Dan Sibinski with Keller Williams Classic Realty joins the show to discuss whether or not we’re in a housing bubble. Dan discusses the housing market trends in Minnesota, with a deep dive into inventory, interest rates, and how those affect the market.

There are a lot of numbers and trends discussed during this podcast, and it will greatly help to follow along with the graphs and charts posted below.

TRANSCRIPTION

The following is a transcription from an audio recording. Although the transcription is largely accurate, in some cases it may be slightly incomplete or contain minor inaccuracies due to inaudible passages or transcription errors.

Bill Oelrich: Are we looking at a real estate bubble? Are we approaching a 2008 experience all over again? It seems like history repeats itself in seven to 10-year cycles.

[music]

BO: Welcome, everybody, you’re listening to Structure Talk, a Structure Tech presentation. My name is Bill Oelrich, alongside Tessa Murry and Reuben Saltzman, as always, your three-legged stool, coming to you from the Northland. We’re happy today to have a special guest with us, Dan Sibinski from Keller Williams Classic Realty is here. Hey, Dan, how’s it going?

Dan Sibinski: Good, thanks.

BO: Awesome. We’re gonna dig into a conversation that we’ve been talking about a little bit around the office, are we looking at a real estate bubble? Are we approaching a 2008 experience all over again? It seems like history repeats itself in seven to 10-year cycles. So we’re gonna pick Dan’s brain today and see what he’s thinking, what he’s seen out in the marketplace, but before we do that, Reuben, and Tessa, you better say hello to everybody, I’m sure they’re patiently and anxiously awaiting your tunes.

Tessa Murry: Hello, Structure Talk audience.

BO: There you go.

Reuben Saltzman: I’m anxious to hear what Dan’s got to say about this, ’cause everybody is worried about this right now. I want you to wax on everything, Dan, I want you to tell me if lumber prices are in a bubble right now.

[laughter]

RS: Seriously. You go to the store, 2x4s are selling for like what, seven or eight bucks right now? It is crazy, so I want you to use your crystal ball and tell us about all of this and where it’s going, Dan.

DS: No problem. First, at least we can scrub out the potential of anybody trying to sell that stuff off-market. You know how hard it is to carry 2x4s under a trench coat? It’s not gonna happen.

[laughter]

BO: I’ve tried.

[laughter]

BO: Okay, so Dan, tell us, we can bury the leader, you can come right out. Where are you at on this whole thing? Do you think we’re in a bubble?

DS: Maybe. We have some predictability that we can look at with that, a glass case of emotions, more than likely, yes, for the buyers out there. Am I able to share my screen with you guys so you can see some of the stuff that I put together for you, in terms of what I use for my communications with buyers and sellers alike? Because this topic comes up almost on every conversation, and if it doesn’t, I like to bring it up because I think it’s very important for buyers to understand right now where they’re at in the market and what they are purchasing, ’cause you can always purchase wrong, no matter what market you’re in, it’s just how you purchase now is the name of the game.

RS: Please do. And whatever you share, I’ll be sure to put this in our podcast notes so anybody can follow along at home.

BO: We call that responsible podding. Sharing a screen to an audience that’s listening sometimes is a challenge, but we’ll back up on the back side.

DS: I’ll use my hands less, if that helps.

[laughter]

BO: Okay, fantastic. [chuckle]

DS: To understand where we are in the market and how real estate itself turns, you have to understand, really, the three key components of what makes up a real estate, which is supply, demand and affordability. Now, as Bill mentioned at the opening of the show, it seems like things change every seven to 10 years, you’re not too far off on that, Bill. Typical numbers between real estate is, anywhere from six to eight years, the market does something different, and why is that? Is it because we’ve got new people in the office, new people making decisions, new policies? Is it because of those policies now our GDP and the industry and job markets do something different as well? All of that stuff has a trickle-down effect to the real estate market, but when you get down to it, the market is controlled by those three factors. Keep in mind, I’m not an economist, I’m not a loan officer, I’m a real estate agent, so these are my opinions, and maybe I’ll be labeled as crazy 10 years down the road, but right now, I feel like I’m that meme that’s out there with the lemonade stands, and I think we’re here, change my mind. So let’s start looking at what these charts mean and how the general public can understand and really watch the market for its next turn. Has anybody here heard the term “absorption rate” before?

TM: No.

RS: Yes, with paper towels.

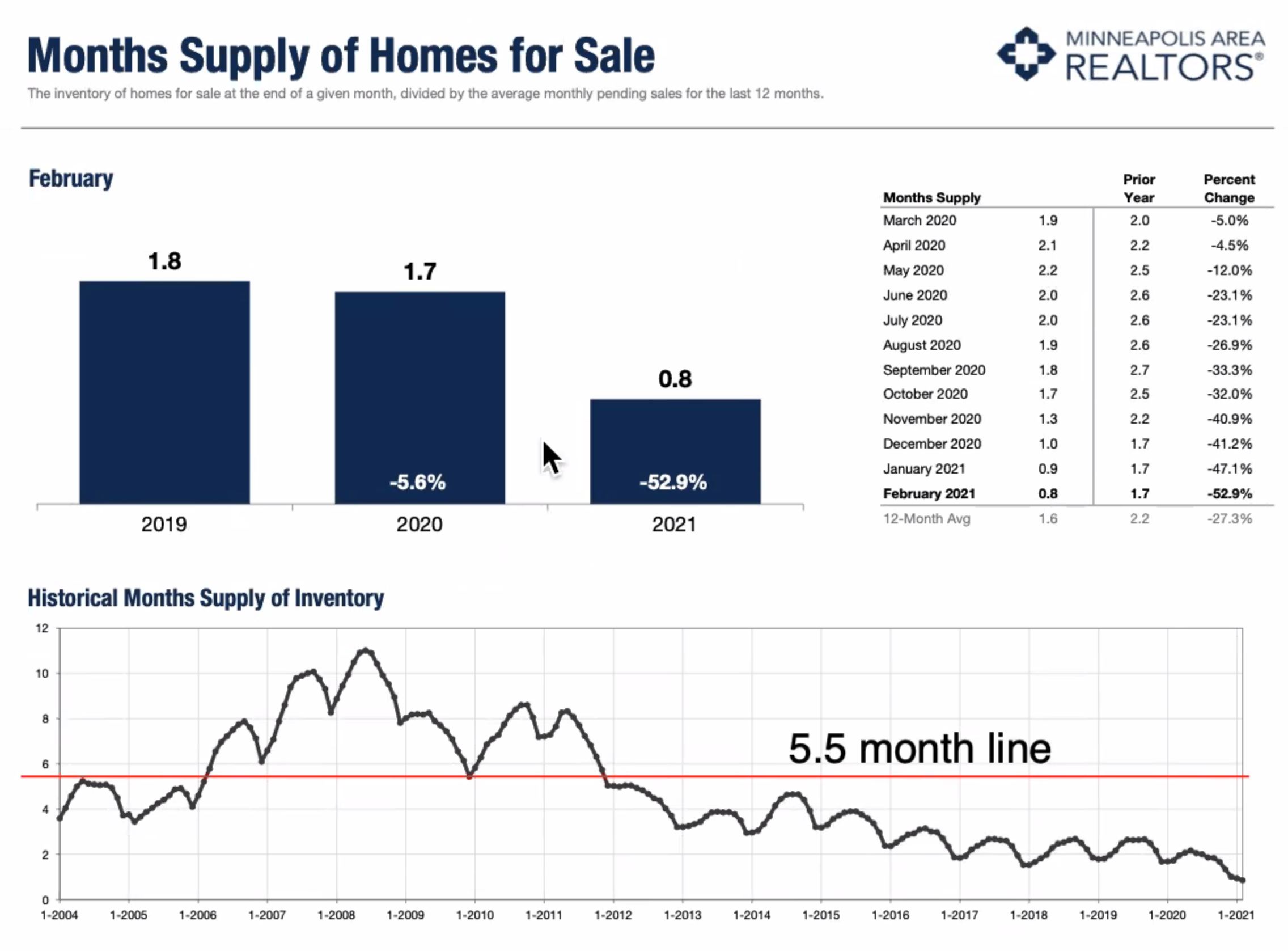

DS: So in real estate, the absorption rate is where they deem a balanced market. Are we in a buyer’s market? Are we in a seller’s market? How is that measured? It’s measured in how many months supply we have of inventory at that period of time that we are in, and if we add no more inventory to the market at the pace that they’re selling, how long before everything is gone? So depending on who you talk to, they’re gonna tell you between five and six months is that balanced market, you got a little room to move on both sides of the fence before you go, “Hey, I’m now in Wisconsin,” or “Now, I’m in Iowa.” You’re stepping over the line. So if you look at this month’s supply, I’ve got a red line drawn in there at where I feel is about the five and a half month line, and I’ll tell you why that’s important here in a couple minutes. What we’re gonna focus on in this conversation is the fall that we had from 2005-2012 and the gains that we’ve had to now. What a great thing, to be able to actually look back on right now and go, “Okay, well, these are the reasons why the housing market changed then, what happened to those key components, and where are we at now, and how is that gonna come into play?”

DS: Right now, you can see my cursor’s down at the 2021 year, and we are at about 0.8 months. Now, the charts that I’m showing you are from February, I know we’re in the cusp here of May, things are gonna trend up a little bit, but some other charts that I’ll show you, you’ll know exactly what those charts look like, but I didn’t have time to put together the fresh stuff. Five and a half month line here is balanced, is the tipping point, and we’re at 0.8 months with all the inventory that we have, 0.8 and everything is gone. I can say it one more time for the dramatic-ness of it, but I don’t think it’s needed.

BO: 22 days worth of inventory.

DS: Correct. Now, imagine how much your house would be worth if everybody knew that number and were playing their odds based off of that. It’s like Armageddon for homes out there, and we’re feeling it, and that’s where you’re hearing all the stories in terms of how radical the market is, how much more people are getting for their homes, the contingencies that are built in for extra monies. There’s a reason why that’s happening, and there’s a reason why it won’t happen eventually as well.

TM: Hey, Dan, can I just mention one thing about that graph that’s kinda interesting? So on the horizontal axis, it’s the year, and it looks like it starts at 2004 and it goes to 2021, and on the Y-axis, what is that, the months?

DS: That’s the months.

TM: The month’s supply of inventory? So what’s interesting is that, from 2013 until 2021, that month’s supply has been less than what you’re saying would be the ideal amount, 5.5 months. It’s been less than that, and it’s been kind of slowly decreasing ever since 2014-15, it looks like. Is that true?

DS: Yes. That is true. When we look at when the median house value started to tip, and we’re gonna get to that slide, actually. You’ll know why I’m putting that five and a half month line in there, why that number is so important to me. And if you remember last year when we were talking about withhelds and this certain percentage of the market that is not in the public size, and what that means from a percentage and how this comes into it, there’s so many rhymes and reasons of why the housing market is what it is right now. A lot of it’s natural, some of it’s artificial, but the game has changed to where, are we gonna get that past time, that past normal back? I don’t think so, which you’ll get my whole round up Nostradamus ideas at the very end. But take a look at this, when the market really started to fall. Look in 2008, I think that’s the year when the government started putting in that incentive, the $8000 buyer credit to get people back into the game. We had almost 11 months worth of supply in the Twin Cities. I mean, we were swimming in inventory. What that means for the number of homes? ‘Cause we have 37, close to 40,000 homes on the market at that time. Right now, with that, well, in February’s charts, that 0.8, it’s showing under 5000 units, 4670 units on the market for all of us to enjoy.

TM: Oh my gosh.

DS: For all I was looking to purchase.

TM: Is this for just the Twin Cities, Dan, or is this all in Minnesota?

DS: Well, it’s a good question. I’m not sure if this is the whole area that the MLS reaches, or if this is the seven metro area. I’m gonna default to the seven metro on it and just hope that it’s right. If not, that’s where you put the Bose on no’s on me and amplify the sound.

TM: Wow, but that’s crazy, from almost 40,000 units on the market back in 2008 to less than 5000.

DS: Right. So I look at this chart and I go, “If I were to look at one of the metrics in terms of are we getting closer to a balanced market, if I was an investor or trying to time the sale and knowing what this might mean in terms of how to leverage myself better as a seller or a buyer, I’m paying attention to the month supply. I’m also gonna pay attention to how many units do we have to play with.” Population growth has gone up since 2007, so I would predict that this number to serve that greater population that we have now is gonna have to increase as well. So maybe we’re looking at a 2500-unit metric, maybe it’s a little over 25 to get to that balance market, if you will. I do know that even if we get back to two months supply, buyers are gonna think that they have it good again. So let’s look at the median price. This chart is super important to me. For those who are thinking that the housing market follows the stock market, “Oh, it’s gonna crash. It’s gonna fall.” Okay, let’s say it is. It’s not like a stock to where it’s gonna just turn down the dial the next day. This thing doesn’t turn on a dime, it turns like the Titanic. That’s a fact.

TM: Titanic didn’t really turn that well. [chuckle]

BO: Tessa. Jeez.

TM: Sorry. I’m sorry. I’m sorry. That fact. [chuckle]

DS: This is true. So I put all three of these charts on the same page, so you don’t visually have to go back and forth, but you follow the line five and a half months, and you look at the market saying, “Hey, something’s not right here. Something’s gonna change.” We’re not doing the normal things that we’ve been doing with inventory. I wish this chart went back to 1999, so we could show all the new construction that was going on and the deficiency that we had in housing and why the prices started going up, but look what happened. Keep in mind, too, during this time, from 1999, that time, we had lots of factors in the market that we don’t have now. We had unverified income, people who were qualifying their home based off of what they said they were making. That doesn’t exist anymore. You had people who were robbing all of their equities out of their homes and maximizing the money that they had on paper turning into a real money in their pocket, making it easier for them to walk away from their home from.

DS: And they were doing it for various reasons, but it was being done at a very, very high level. Even that right now is being held at a comfortable rate, let’s say. So the fear of a foreclosure market happening right now, it’s not really existent. And I’ll tell you what, even if it was existent, there is such a low amount of inventory, let those people go into foreclosure, and that inventory is gonna get swallowed up because we’re so under-fed right now in inventory. Plus, quite frankly, if people are losing their jobs, if the job market isn’t supporting employment, if we get a big change in that area and people do have to go through foreclosure, it’s a 12-month process in Minnesota, and they’re probably sitting on equity, especially if this happened within the last year ’cause housing values continue to go up. If they’re missing their payments, they’re not qualifying for any heloc or any money to take out of their home, so they’re kind of self-protected in the market that we’re in right now just by default.

DS: I think the lender mitigated aspect is gonna be very nil. There are numbers with FHA mortgages being that they’ve all been suspended in terms of foreclosures, that maybe there might be a wave of them coming, but the last chart I have to show you is the percentage of FHA mortgages that are out there, I don’t feel it’s enough to put a dent in the market. So again, you look at how long it took the market to figure out from a median sales price that something wasn’t right before it started taking the dive, and then in 2012 when it hit rock bottom and inventory fell below that five and a half month line, we’ve been on this wave of equity gains and, Bill, we are over that eight-year, we’re getting closer to that nine years. We’re gonna get into that 10th year.

BO: The charts are awesome, but visually speaking, what you were explaining before, that correction was happening over five years, back and forth. It was just this nice wave, and now it’s just this very long wave going down on inventory in this very long upward gain on the median sale price. So that gap can’t be good. [chuckle] Just visually looking at this.

DS: Yeah, you would think. It’s hard to say if it’s good or bad. Is it gonna be corrected is the question, and if it is, by what degree? And then, how long is it gonna take to get back up? We can all look at a historical chart of 50 years, 100 years of real estate, and know that over the long run, you don’t lose. It hasn’t been proven to be a loss yet. You try to buy it off the market in these two to three-year grasps, and that’s where the problem lies. Because especially if you’ve been in this kind of market for eight years, nine years, it’s more natural to say, “I’m getting close to the turn.” Where if you made this decision in 2013 or ’14, you had plenty of time to ride that wave and make your decisions, and that’s where the conversation comes in with buyers is, “What kind of home are you looking to stay in?” I have a 10-plus year conversation with my buyers that is really one of the biggest things that they should focus on in terms of how long they plan to own their home, and I’ve got charts for that too, will put that conversation into a better light.

TM: Can I ask you a quick question? Do you think that that standard 8-9 year cycle that you were talking about is consistent across the country and other states as well? Or is this just Minnesota you’re talking about?

DS: For now I’m just gonna say, is Minnesota. I know everybody else has their own cycles. We have an agent that I’ve been communicating with, and she says that during the downfall in 2005-2012, Colorado didn’t really have the same experience; Texas didn’t really have the same experience. Some of these larger states had to have these amenities that are less found in other states, and they have their own economies, almost. You look at Texas, there’s talk about them being their own serviceable country, or California.

BO: Yeah, and then you look at those, I don’t wanna call Texas a micro-market, but they’re one of 50 in the states, obviously, but then you have the influx of people coming from, say, California; Texas is being called the new Silicon Valley, right? Austin is this kind of booming area, where the whole Texas Triangle, the Metroplex, there’s a lot of people pouring in there ’cause it’s favorable for taxes. So people leave California and they’ll go to Texas; they get a similar weather pattern, something like that. So you have all of these occurrences for the why; it’s not always transferable completely across the country.

TM: Mm-hmm.

BO: Right.

DS: Yeah. So a couple of other thing I’d like to point out and that come into play with my predictions of the market; there is a lot of stuff happening over here that’s not happening now, okay? Things that could really negatively affect the housing market. So looking back at these charts, I think it’s really important in terms of shaping my conversation in where I think the market’s going, is you gotta look at what was happening in certain time stamps; you go, in the ’90s to 2005 when the market was leading up, you had all those things that shouldn’t be happening, the unverified incomes, the straw buyers, all the things that shouldn’t be happening. And then you had the foreclosure crisis, which was just an after-effect. The stuff that was born out of that is renter’s warehouse; you have all these assets that came in; you had all these group bulk money that was going into metropolitan areas; buying up tons of homes for dirt cheap, pennies on the dollar.

DS: It used to be where people would own their homes for an average of 6-7 years; now that number is closer to 10-11, and some of these numbers in my opinion have to be swayed by the longevity holds of the investments, ’cause there’s no reason for them to sell it, especially at bulk money when they had to have such a low price, and the way the appreciation has been happening, increasing their portfolio’s value to where they can leverage it against other purchases; that’s happening. Then you also have everyone who bought in the low end, from 2012 to now, that’s gaining so much equity. We had interest rates back in the early 2000s that were near seven; we bottomed out at 2.75%, making the thought of anybody trying to refinance out of that rate, and tough question and a though decision to happen. And then you go, “How does all that work and how does it all plug into each other in terms of the housing bubble and how people are gonna make their moves?”

DS: I find it really hard to believe that people are gonna walk away from it, especially when the rental market now, it’s still in a lot of cases, still more affordable to purchase because of interest rates than it is to rent. Remember when everybody let their homes and go, back in the mid-2000s to almost 2010; it’s not like everyone just vanished, like, end of the infernos, like you snapped your fingers and all these people went away; they still had to live somewhere, so that put extra pressure on the rental market. Rental rates went up, rental vacancies went down. The same thing technically would happen if we had a foreclosure issue due to massive job loss, world war, or something crazy happening that is really unpredictable. The rental market’s gonna be great; believe that long-term. And I think that’s also why people are holding on to their rentals; I also think that’s why people that I know that I never assumed would be a landlord are also now choosing to buy a secondary home, ’cause the numbers still make sense, and they’ll make even more sense when they go over the charts that I put together for you guys to view.

BO: What’s gonna be the factor that tips this one way or another?

DS: Interest rates. I look at it as three to four things from my knowledge and my guesstimentation that is gonna make this market change. You’re either gonna have a much more harder pandemic that comes in and it’s less forgiving, even though COVID’s been really tough on a lot of people for a lot of different reasons. But imagine a pandemic coming in that wipes out 20% of the population, and now we have housing available for the wrong reasons; that would be a game changer for inventory. Assuming that’s not gonna happen, you have to go, “What’s next?” Well, job loss; job market; something big in the world happening to affect that. What are the chance of that? Unemployment’s actually pretty good right now; it’s been really good and hopefully it’ll stay really good. So then you have interest rates, and they have been rising; we bottomed out at about 2.75. Now we’re at, I believe, we’re roughly around three-and-a quarter; historically great, but when you look at the numbers and how that affects your affordability, and you look at the buyers who are maxing out at, let’s say $300,000 or $400,000, if it moves a point, you’ve now just lost about 10% of you purchasing power.

DS: So the buyers who are maxed out at $400,000, now they can only qualify for $360,000, so the inventory will naturally start growing slowly, and that’s where you start seeing that slow trend. Once we get up to those numbers of 5-1/2 months, you’ll see that slow trend in the median start to kind of pan out, and is where I think that goes. From there, it’s interest rates; how much inventory do we have; and then how competitive do sellers need to be at that point in time. But we’ve got a long crawl to get there. Pulling aid, even if it’s one-and-a-half month’s worth of supply, I’m thinking this is years. When do we get there; it’s gonna be interesting to see what kind of stimuluses they put into the housing market to try to curb it, because I think that will happen too.

BO: Yeah, it’s interesting, ’cause I just don’t see that the people in charge of the interest rates have any appetite to see them back up at the early 2000s when we bought our house, our rate was at 7.5% and it kept falling over time. Obviously, I kept thinking, it can’t go lower, it can’t go lower. But I don’t see an appetite for politicians or anybody else who’s connected to interest rates to see them go back up.

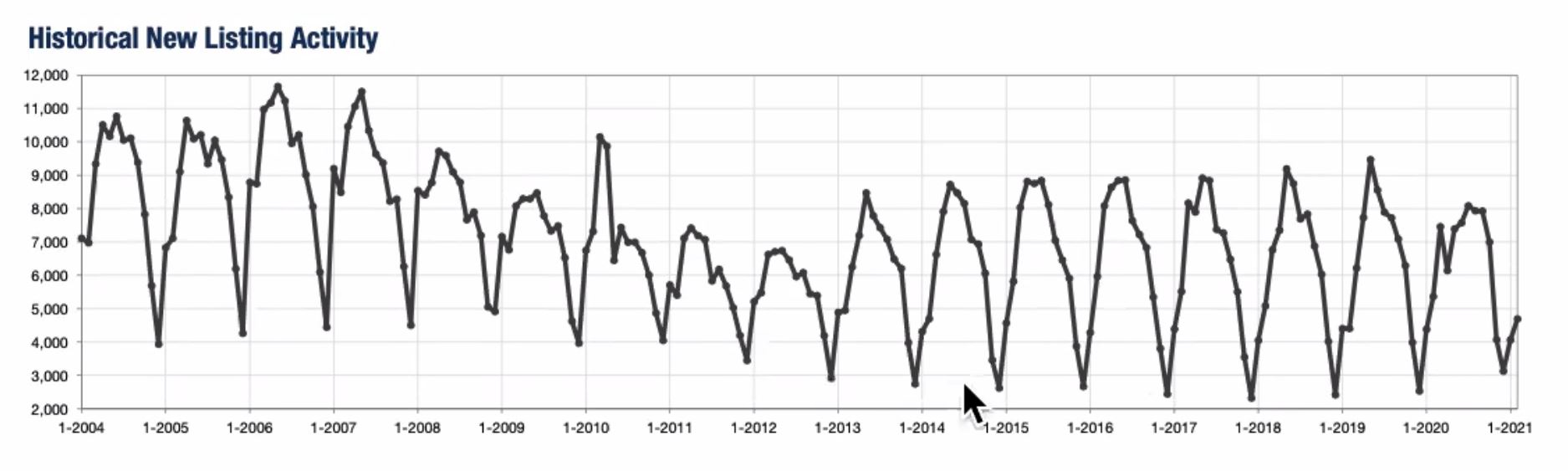

DS: Correct. So if we concentrate on interest rates next. I’d wanna do with you as buzz through the heartbeat of Minnesota in terms of bad market, good market, where does all the inventory come from, when does it come into the market and where do the buyers fit into this? So when looking through this chart of 2004 to now, whatever market we’re in, you can see that most of the decisions to list typically happen in December and then inventory grows, and it typically spikes in about May to June. You take away realtors and everything, the activity is what creates this chart, and this is what’s happening. We’re just blessed to be able to see it and follow it, and you can see what the housing market did last year in COVID, where we started to do our natural trend up, and then we started to have the lockdowns and then people pulled their homes off the market for two to three weeks, and then everyone realized we’re not the stock market, and guess what, people need to move still. So then we have that little double peak, triple peek, if you will, before following that natural footprint, getting back to December bottoming out, and now we’re right in our crawl back up.

DS: The buyer activity, same. They follow the same footprint as the sellers. Everyone’s making their moves, their savings towards the end of the year. We’re gonna start afresh in 2021. If you look at all of the buyers as a full spectrum, you’re gonna have people who are wanting to get into school districts, make their move before summer hits. Minnesota has got very short summers. Once I’ll take a pause to really understand that. End of graduation time people have parties, they have gatherings, you get a short reprieve until the 4th of July, more trips centered around that. Then it’s back to business before the state fair hits and then school starting. You can see pending properties still happen, but it happens less. Less competition, less stuff to look, less activity. Closed sales is just a natural progression of the actives and pendings. I was listening to a couple of your other podcasts and there were some interesting conversations regarding what markets are seeing the most amount of activity, which ones are the most affected. They really can chunk down these numbers.

DS: What we were just looking at is like a 30,000-foot view. Now, in these charts, I have the ability to break it down to different price ranges for you. One of the hottest price ranges is that 350-500. And you can see year over year we’re down 53.6% and available pre-owned properties, not including new construction. New construction has been on the rise, which is great, ’cause they’re meeting the inventory with that previously-owned, down 53.6%. Absolutely amazing. And then you look at the buyer pressure. It’s up 25.9% in that same price range. Extra squeeze, extra juice. If you look at how powerful these interest rates are into the conversation that one million price range and above, up 36%. That is the actually the highest yielding year-over-year growth in purchases, plus-a-million. Month supply for that million-plus, 3.7 months supply. That number should be 10-12 months plus from the pure affordability aspect.

BO: Sure. Money is cheap.

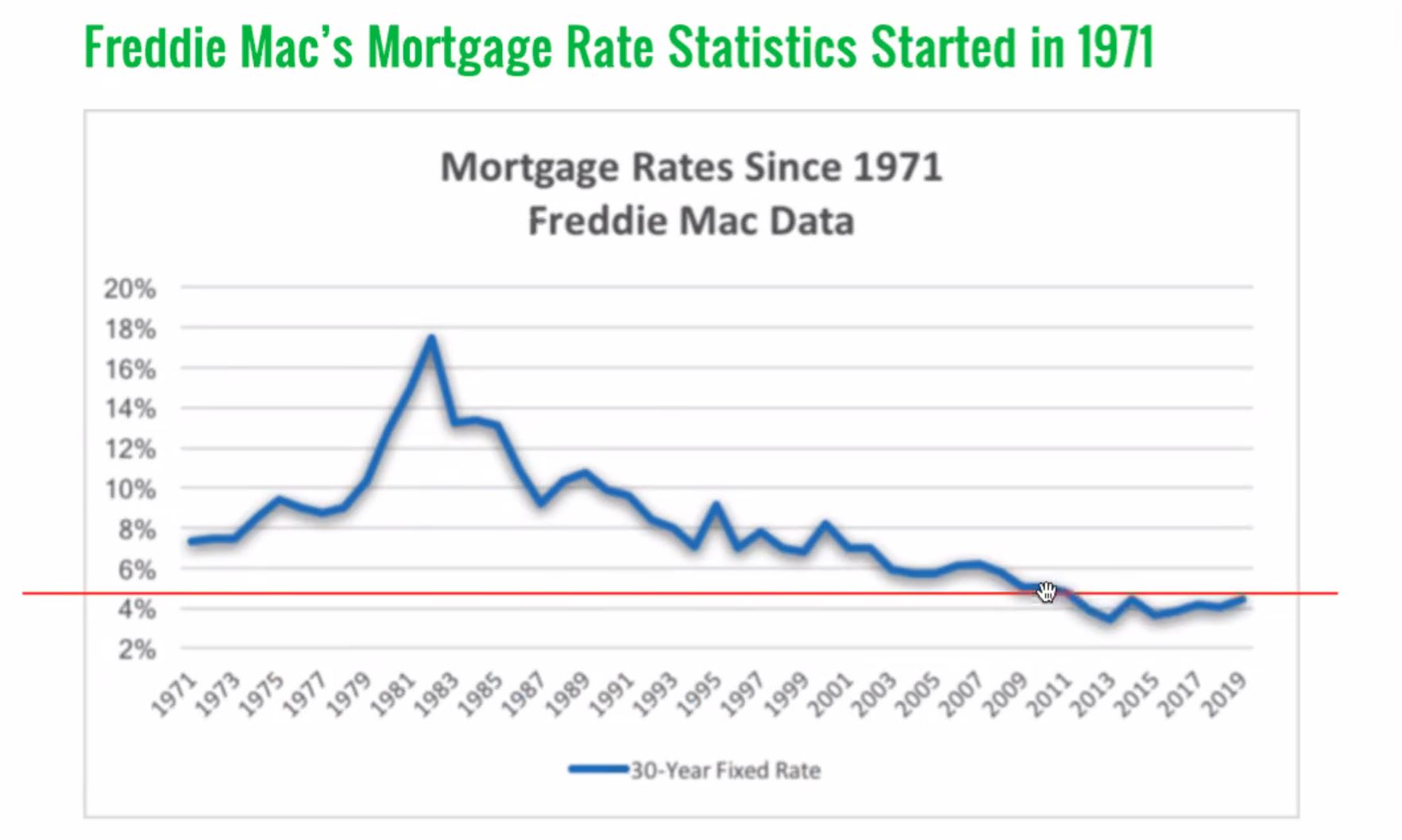

DS: Yeah. It’s almost free. And when you look at these charges for the mortgage calculators that I put together for you, you’ll see the power of it, and this is why it all makes sense until it doesn’t. This graph right here for you shows us the best of times, the worst of times in terms of interest rates. Goes back to 1971. The early ’80s, TV was great, growing pains, family ties, but the interest rate, not so much.

BO: 18%. I can’t even imagine. [laughter]

TM: Wow.

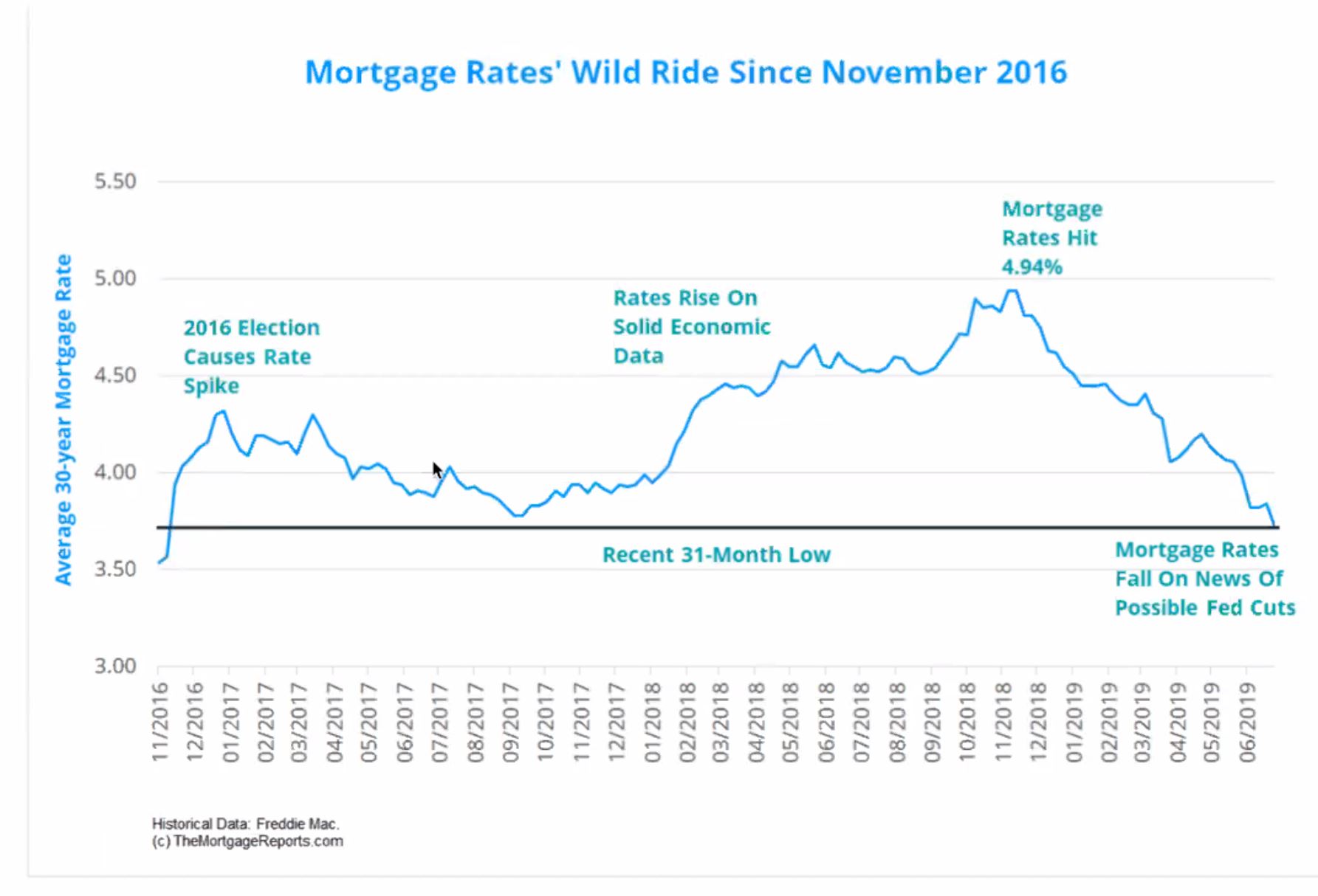

DS: When you look at when that market started to change in 2012, notice how the affordability line, even from 1999 to the crash, it started dropping, but we were still at around 8%, 7-8% when the housing market went on its last previous run to the last previous fall. This is a chart that I think is also important from 2016-2019, it shows our dance in between three-and-a-half to where we almost hit 5%. There wasn’t a conversation that I had with agents back in 2018 where we didn’t think this wasn’t the shift.

TM: And you’re talking, just to clarify, you’re talking mortgage rates.

DS: This is mortgage rates, yes. And because affordability is such a big factor the conversations within our industry was, “Here comes the shift. We’ve had a good six-year run. Here comes the shift. How are you gonna start doing our marketing, our conversations and educating our clients?” But then rates ended up falling back down. If I were to scroll back one of those earlier charts about the median value and where that was at and how everything still increased, there was nothing that showed up on the radar that said, here really comes the turn. It was a small flattening out of the median for about four months, if I remember the chart right, and then we started climbing back up again. Now what that means? And this might be a little harder for me to explain all the numbers through the podcast. I’ll do my best with it. This is the power of money right now, and where it could go. I don’t think anyone here, or listening, is gonna argue that getting back up to that 5% is gonna be something that we’ll never see. We’re definitely gonna see it. But what does this mean in terms of payment now versus your principal and interest and what you start out with and what you end up with at about 10 years?

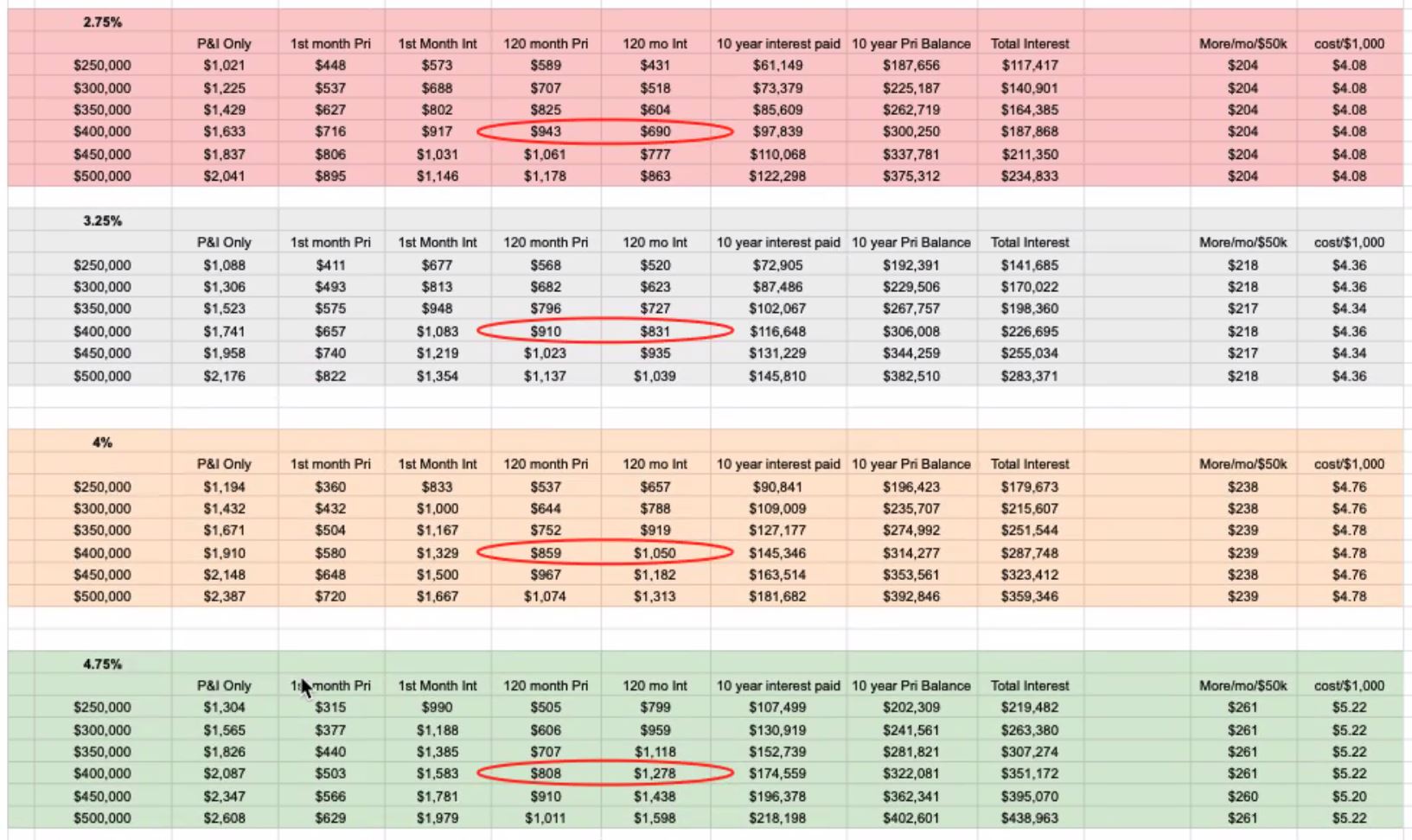

DS: And I use this 10-year mark, because right now that’s the average lifespan of somebody owning their home, which I believe is gonna change. So let’s look at this price range of 400,000. I’ve got four different charts for you to see the 2.75, 3.25, 4% and 4.75%. When you look at your mortgage payment, just principal and interest only. This isn’t taxes, insurance, PMI, nothing like that. I’m not a loan officer. I used a loan calculator for this. Everything that we can use from the general public. You put in a $400,000 mortgage and your principal and interest is $1741, starting out at a $400,000 purchase at today’s rate, 3.25%. From an investment standpoint, the market’s gonna do what the market’s gonna do. From a you standpoint, you have that interest rate for as long as you own that home. And if you’re there longer than 30 years, that interest rate goes away, that mortgage payment goes away. Now, banks aren’t stupid. They are here to make money off of you, and they understand that people sell their homes typically within 10 years. So guess where you pay the most of your interest? Upfront, those first 10-15 years. You look at that 400,000, that first month payment, $657 is going towards your principal. You’re paying yourself back for being a home owner in the bank is making $1083 off of your payment, starting out.

DS: Every month this changes. Interest goes down, principal goes up. Now, if we’re all gonna take a vote, and we all agree that we’re gonna still be alive in 10 years, and we’re either gonna own a home, or we’re gonna rent a home, if you’re renting, that money is just gone. If you’re owning the home, you’re paying your principal down, you’re getting a nest egg, you’re gonna go through one or two real estate cycles, that’s gonna be what that’s gonna be, but your balance is gonna change. Take a look at this principal, at 120 months, you’re 120 month payment, you are now paying $910 towards your principal, versus that 657, and you’ve tipped the scales, it’s only 831 towards that interest. Imagine if you put a renter into your property at that point who is covering your mortgage, they are paying your principal down 900-plus dollars every month starting out. Now tack on the natural progression of real estate to where over that 30-year span you can possibly count on that 1.5-2.5% appreciation over that time. Seventy-five-ish percent on one of the statistics I’ve heard, 75%, roughly, of the equity, of the riches, the wealth that people have earned has been through real estate. This is why the long game works out. How you purchase your property works out.

DS: If you’re talking to buyers right now, and they wanna move in two to three years, not a great decision unless they understand the risk and reward potential. But if they can commit to being there 10 years, this is math, this isn’t my opinion, you can tell them where they’re going to be on the map. And you look at what this also means in terms of principal savings, now, this is the 3.25% graph, so in that 10 years you’re gonna pay $116,648 in interest. Looking at 4.75%, for those who are going to wait and time out of the market and purchase when the housing values go down, guess what’s gonna make them go down? A higher interest rate, higher inventory, but until that happens we’re gonna have appreciation. But let’s just assume we’re looking at the same house, same cost. On a 4.75%, your monthly payment now goes to 2087, versus 1741. Your first month principal is only 503 bucks, versus the 657. Interest is $1583, versus the 1083, $500 more you’re paying the bank for the same home that you wanna live in and own as an investment.

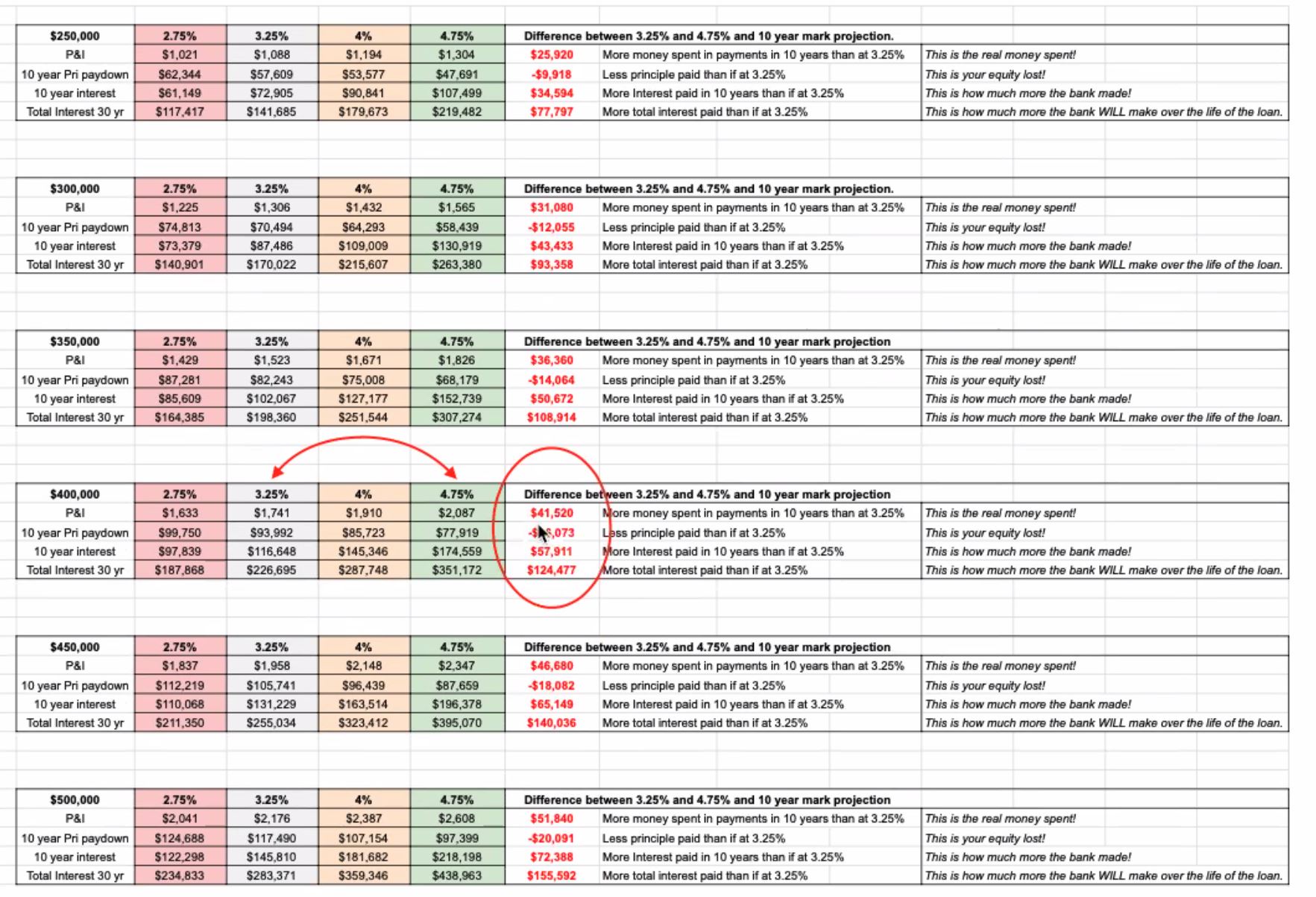

DS: At 10 years, you’re not even close to tipping the scales. At 10 years you’re now $808 for your monthly principal pay down, starting out, and you’re still at 1278. Your principal and interest always stays the same, remember, it’s these numbers that change on a monthly basis, but you are gonna spend a lot more money. This next chart I tried to bring all the numbers together to make it a little bit more digestible. If you look at the difference between the 3.25 and the 4.75, over that 10 year run, your principal and interest payments, you’re gonna spend $41,520 more out of pocket over 10 years. You’re also gonna pay yourself down less principal in the amount of $16,073; $16,000 less in your homes equity by trying to wait this thing out. You’re gonna pay $57,911 more in interest during that time. In 10 years, imagine getting somebody giving you $5709 every year just because you made a decision to purchase earlier. This is exactly what’s happening for those who understand the numbers now. Over that 30-year interest you’re gonna spend $124,000 more in interest. These numbers are powerful, they’re real, they will happen eventually. Where the housing market is at that point, really hard to predict, but this is one of the big reasons why you have all this extra pressure on the market right now.

DS: And how this ties in, for me, is you’re gonna have all these people who have a rate that’s three and a half and under, those who have refi into their current position, it takes five years to get to where this 4.75 is, maybe less, maybe more. There’s gonna be those who absolutely have to move, but there’s gonna be those who understand the market and that they’re sitting on a potential investment retirement vehicle. And there’s gonna be more entities that come to the market that make the rental process easier. You’ve got younger generations that absolutely love moving jobs and locations every two to three years. I can see the housing market having certain sectors of housing be formfitting just to that, two to three-year leases, people can work remotely. In my opinion right now, unless something drastic enters into the market and changes my viewpoint, I think the haves and have-nots in housing in the next 5-10 years is gonna be a very, very distinguishing thing, and those who understand the numbers now, you’re giving away a little future equity sometimes to get into the house that you want, but if it’s long-term, it doesn’t ever.

BO: Is this a really a bubble there, or are people just not moving out of their houses?

DS: I wouldn’t say there’s a bubble as much as I’d say there’s a shift, ’cause the market shifts. It looks like a bubble because you can track the charts and stuff, but it’s really just these cycles that we go through. And we will get to a change, it’s just a matter of when. And part of the, I don’t wanna say a funny thing about the market is, is that very few people look at the historical aspect of real estate, but they do understand that they need to live somewhere. It is just survive. And you gotta survive. You have to live somewhere. You’re gonna wanna get out of your friend’s place, out of your parent’s place, you’re gonna graduate into the next stage of life, and you’re only gonna know what you know at that point in time. So those getting into the market when it’s 4 1/2%, or 5%, that’s all they’re gonna know. Everything else that surrounds it, that’s more of the bubble to me, what’s gonna cause the shift.

TM: So Dan, do you think it’s really risky then for people in this current market to be offering 10-20% over asking price?

DS: So I love this question a lot, because the list price of a home is a price opinion. It’s all it is. It’s good enough to get your eyes on it, it’s good enough to get your attention, it’s good enough to get you into the home. It doesn’t speak on what time of the year you’re in, it doesn’t speak on all of the chart information that I just showed you, and being able to understand the market and where your leverage points are, and quite frankly, it doesn’t speak on the comparable comps from around that subject property that you’re offering on. I’ve seen so many properties enlisted low for different reasons, it could be just a mix-up understanding the market, or it could be an agent trying to enlist them low for, I hate to say a quick sale, but sometimes bragging rights. Outside of 2021, in what the market’s doing right now, if you’re getting more than $20,000, more on a $300,000 listing, you probably underpriced it. There is an unpredictability factor to this market though because there’s a lot of money that’s coming out to play. ‘Cause I’ve listed a couple to where I’m like, “Okay, we’re probably at the point where we should be concerned about an appraisal,” but you still get that 30 over, but it’s how it comes together versus why.

DS: And it’s because the rates, you gotta understand, the rates are going up, the conversation surrounding that for those in the purchase position are hearing it and understanding it, and more of them are coming up to bat, and it puts more pressure on that moment and on that market, and it raises the unpredictability factor of that performance. But eventually, that goes away. We’re hearing all these crazy stories going from December until now, but based on the charts, this is also where we live in the lowest amount of inventory. We have 30% more buyers that are pre-approved this year than there were at this time last year. A lot more people entering the market, putting more pressure on it.

BO: What you’re telling me is that people are buying houses, they’re staying in ’em longer, and when it’s time to go buy another one, they’re not always selling the house they have, they’re just converting it into a rental agreement, and they’re cashing in on somebody else paying a bigger chunk of their principal payment off each month. That’s just amortization, that’s how it works, you always pay interest on the front side. If you keep refi’ing all the time or when you refi when you’re eight, 10, 12 years into the process, you just start back at zero again, start paying a lot of interest.

DS: You do if you’re refi’ing into a 30-year. I myself, before rates hit a rock bottom, I had 20 years left on my 10-year mortgage, I was at a 4.625 interest rate, I refi’ed to a 3% on the 20-year, lowered my payment, lowered my interest, and I’m saving close to $80,000 over the next 20 years just by refinancing correctly. Again, what’s the percentage of people who understand the numbers and are looking at everything other than that instant gratification of, “Hey, I just now got this lower payment,” and not understanding what they might have done on the back end in resetting their clock? There’s potential for a lot of bad decisions to be made, but for those who have refi’ed regardless into that 2.75, was 2.4, 2.5, even 3.5, it gets really hard to walk away from, especially if the rental market is so strong to where you can cash flow on a mortgage, plus your principal reduction, plus forecast your appreciation at a bare minimum. That’s where the investment conversations come into play.

DS: This last chart, it maybe throwaway information in terms of our conversation right now, but it is interesting when talking about strategies with sellers and buyers alike in terms of what their competition is, and how we can leverage offers in the multiple offer game. Where these buyers are coming from in terms of the financing? Up to last year, we ended roughly around 73% were conventional purchases. Their next leading contender was cash, 12.6, cash, all price ranges. I’ve lost out on $500,000 homes this year to cash.

TM: Wow. [chuckle]

DS: I don’t know where this money’s coming from but it’s out there. Secondary properties up north, on fire, 8.9% FHA. FHA is a different kind of loan, we could talk about that for a while, but the only thing that’s sexy about that FHA potential, and you’ll be able to replay this podcast maybe in five to 10 years, whenever interest rates start getting up to that 4.5-5%, FHA is the only one that is assumable to where the next buyer can actually assume that mortgage and assume the terms left in that mortgage as well. So anybody who’s locked into a 2.75 on an FHA, if rates go up to 4%, and the next buyer, if they qualify, they can take over that 2.75, have 20 years left on their mortgage, awesome principal paydown, they just have PMI to worry about. But eventually, the numbers just makes sense. And then you have other properties mixed in there, probably VA and rural stuff, and then some distress sales as well. But this is where you would typically market to, property condition, who you would expect to come into your home in terms of offers. I can tell you the FHA offers, they’re the ones that are getting beat up left and right right now. Unfortunately, between the haves and have-nots, in terms of money being available for purchasing, you’re gonna have buyers that come in that don’t have much of anything more to put down than the bare minimum.

DS: Maybe they still need seller contributions, but they are coming in hot and heavy with their offers, and it’s often flexing the escalation clauses up to their max levels. The micro-strategies involved there are a completely different thing to talk about, but all this stuff comes into play in terms of setting those expectations, making yourself a better agent and a better communicator with your clients.

BO: Dan, is this cash that you’re seeing coming into the market, is that some of these cash offers for your house? You see it on TV all the time, “We’ll buy your house.” Is that where that cash is coming from, or is it just the everyday Joe bringing a suitcase full of cash to closing?

DS: Everyday Joe. It’s called fiction. It’s surprising where a lot of this money is coming from. There was some national statistics that I think I heard through our family reunion, or it was through the National Association of Realtors, chief economist, of the people who were affected last year versus who weren’t, and it was the age group of, I wanna say 36 of age and above that had the white collar jobs that are just crushing it in the real estate market right now. But that also means that the need for the others is just pent up and waiting to pop. So even when we start getting more inventory, as long as the affordability factor is there, the job market is still there, that pressure, it’s going to be alive. And again, when does it not affect inventory to where inventory starts to grow naturally? It’s a really interesting circle that I see us in right now to where it’s hard to predict when that change actually comes. And I think it’s at that 4.75 to 5 at these prices, to where I think you just can’t avoid it anymore. The purchasing power difference is gonna be about 15-20% different than what you’re at right now, which is a game-changer in my opinion.

BO: It feels like we could bring on more new inventory too, and that would just be absorbed right up. I’d be curious to talk to a builder and ask him about lumber prices right now and how that’s affected their ability to stay affordable with their inventory.

DS: Well, I’m working with several clients that are purchasing new construction, ranging from your national builders to local custom builders, and it’s actually very interesting that the local custom ones have better turn times. Everyone’s affected by the pricing, the same amount, but these national builders who have contracts with these sub-contractors. So they have a limiting amount of them, but I know some of these national builders, they’ve stopped selling lots. They’re only building spec homes because whether it’s appliances, cabinets, COVID shutdowns with their crews, they’d have this swing to where they’ve had all these delays to where they can’t price protect their profit margins, so they couldn’t build them in the time frames guaranteed that they were originally seeking. So now they’re building specs and releasing the prices once they’re more confident.

TM: The unpredictability has really impacted that.

DS: It’s such an amazing industry and how it swings. Through the foreclosure era to now, very dramatic results between the buyers and sellers, opposite ends of the spectrums, but how it all comes to play together on a micro level is just interesting. So how you buy is super important, why you buy also important, and for how long is really the conversation to be had right now.

BO: Lienholder, that’s what I learned. Once you own that house, you never sell it, just rent it out to somebody else. When you’re tired of it, you just rent it out, go buy another one.

TM: This is just really interesting, Dan, just all of this information and just hearing the reason for the crash back in 2008-’12 and everything that led up to that and how you’re not seeing parallels in this cycle and that it’s probably not going to be a huge crash or a big burst, it’s going to be just more of a gradual thing, it sounds like.

DS: There’ll be a pause. If everything goes the way I think it goes and there’s nothing dramatic that enters the scene, there’ll be a pause and then you would think of pullback. It’s the natural selection if you will, and the pullback might feel a little bit greater because of the things that are going on right now, but we won’t know until we get there. I’d be a fan if they were to give us a little bit more data in terms of the homes that are being sold right now, if there was some simple checkboxes that were added to the MOS just for the professionals’ eyes, realtors and appraisers, that, “Hey, this home appraised or it didn’t appraise.” What great information would that be in terms of making sure that the neighborhood’s value isn’t getting overinflated. And the normal conversation is, it’s only worth what somebody’s willing to pay, but appraisals exist for a reason. There’s gotta be somebody that governs the values because the mass majority of people use financing. The lending institutions say, “Hey, this is our guardian with the appraisal,” and if that data’s not available for them to be able to fact-check that somebody’s putting $50,000 down over cost, set a new bar for that neighborhood that isn’t realistic for the larger percentage of buyers. I think that’s where my attention is gonna go next outside of the withhelds and the hidden inventory again. That’s the one I’ll be paying more attention to.

TM: Is there any data out there that tracks that?

DS: The appraisal?

TM: Yeah.

DS: No, nothing. It’s all individual in terms of the appraisal and the appraisal companies.

TM: From what you’ve seen just being a real estate agent in this market, have you seen a lot of people still offering cash over what the appraise value is and the deal closing and going through? Have you seen that happen a lot?

DS: Yep. So my natural progression and check-down is, if we’re at a brand new home on the market and I’m with my buyers and they have interest, first go-to is the comps. Is this home price correctly? Is it priced over? A lot of the times it’s priced over. It just is what it is. One of two things are gonna happen. Either that home sits, it’s not rewarded, even though we’re in the market that we’re in, and I could pull up 100 a hundred homes in any one of the cities that you live in, and you will find homes that have been on the market for a few weeks, if not longer, eventually, they end up going through the price reduction cycle until they get to market value unless they can get there and they decide to hold it. If you end up in multiple offers, all bets are off in this market right now, if multiple offers exist, even if the home is priced at or above what might be perceived list, chances are if it’s within the first day to two to three days, you’re going over. At that point, let’s talk about the long-term capabilities of this home for that purchaser. Can they grow into it or are they gonna grow out of it? And then what is it worth to them? If we can write an offer and it sticks, great, if it doesn’t, we move on. More business decision versus emotional and just setting the stage so that hearts aren’t getting broken every day.

DS: Same conversation if it’s been on the market for three weeks, they might be in line for a price reduction. Your offer strategy changes and you start talking about the other things. But anything in the first couple days, it’s what that house is worth to you, do you wanna do unlimited dollar amount of an appraisal gap coverage? One of my go-tos is I’ll never ever recommend waiving an inspection, but based on all the things that I’ve learned from structure tech and previous construction knowledge and history, I’ve got a pretty good barometer of pointing a whole bunch of things out. There’s of course tons of things that I can’t see. Carbon monoxide up in the attic, electrical stuff, but a lot of visual things I can point out. So I try to prep my buyers in terms of expectations on cost and what would be in a general home inspection and then say, “Here’s the other things that we can do. I recommend you get an inspection, but I’d be surprised if there’s more than $4000 worth of damage.”

DS: Anything that I can see, you’re probably starting at $4000 and up. So let’s take the bogey man out of the closet for the sellers and say, “We won’t ask for any repairs that fall below X amount,” and if the buyer is comfortable with it, we use that as one of our stepping stones in hopes of getting the offer accepted. On the other side of the fence, you’ve got a seller who’s freaked out about one, the market being that crazy. Is it gonna perform? Is it gonna appraise? Are they gonna be rewarded and then what kind of buyer are you gonna get? So you gotta put as many guarantees upfront as you can right now, which the typical big ones are inspection, appraisal gap coverage, earnest money, what are you willing to walk away from and risk as a buyer? And no conversation should ever be the same with that, it should all be customized to your client.

BO: Are you having all these conversations with all your buyers? Do you kinda sit down and go through this?

DS: Yeah. I rip off the band-aid right away. As soon as we’re done shaking hands, I tell them, “I don’t wanna sugarcoat anything.” Anybody coming into the market has heard the stories anyway, but guess what? They’re here, they wanna buy, and I need to figure out the reason why and I have to be able to educate them as to why it is a good time or why it isn’t a good time for them and be prepared to do what it takes if it’s still a good time for them at the end of our conversation.

BO: It’s like a PhD level education in the Minneapolis market.

TM: Yeah, I was just gonna say it’s, how many agents do you think do this kind of level of education and awareness with their clients?

DS: Very few. I’m fortunate to know a lot of very detailed people out there. But like any industry, you’ve got people who are just starting that are gonna be absolutely amazing as they continue to grow and educate themselves, but there’s a time frame that it takes. You guys train people for, probably, what? Six months to a year, before you even let them go into a home.

BO: Two weeks, Dan, just two weeks and then we set you free.

[laughter]

TM: We’re working on making it more efficient, Dan, we are. We wanna make sure the quality is still there though. Yeah, it takes a while to learn all this information.

DS: When you’re in the real estate seed and you have to answer some questions about financing, lending, how that plugs in, the expectations and the trials and errors and pitfalls that can come from it, title work, the home, the opera process, and all the way through, you are the middle person in the transaction, and now you have the code of ethics and your fiduciary duty, and we’re getting compensated well, at the end of the day, when you do your job correctly. So in my opinion, you should take this as seriously as possible, educate yourself to the best of your abilities and just be that great communicator, put that consumer first, the rest of it falls into place.

BO: That sounds good. So Dan, can you tell everybody where you can be reached at?

DS: Well, I’m with Keller Williams Classic Realty, it’s the Minnesota strong home team. Cell phone number is 763-350-5850, and my email address is Dan.mnstrong@gmail.com.

BO: I think everybody, when they’re listening to this podcast, should download the show notes, ’cause it’s gonna make a lot more sense. There’s a lot of detailed information here. It’s really interesting to look at, but I think we should just indicate that, do everybody a favor, ’cause this will make so much sense when you see it visually. But Dan, thank you very much for spending some time with us. You’re like the professor of real estate. We just get so much information, so thank you. I appreciate it so much.

DS: I appreciate the opportunity to share my thoughts and hopefully when we look back at this in five to 10 years, that at least I hit the board with some of the darts.

BO: Alright, Reuben, do you have anything before we put a wrap on this?

RS: No. I’m letting this all digest. That’s a lot of information, Dan.

BO: Yeah, he’s taking it in. I love it.

TM: It is. It’s a new perspective, and I feel like coming away from this information, Dan, it’s a very different perspective or feeling that I’ve gotten from other real estate agents and other people that are looking at the market too. It’s all based on numbers and it makes sense. So I’m just trying to process it too.

BO: Tessa, it’s all emotion. There are no numbers in this field.

[laughter]

DS: It’s true. If you have the ability to separate, moreso, the why’s of why I wanna buy a house, and I don’t ever wanna rob that experience from a buyer, and in a balanced market you don’t have to be as stringent on your conversations ’cause you’re in balanced market. But if you’re not setting expectations up, there’s gonna be a wide range of emotions and heartache and heartbreak. This market isn’t for everybody. Even with being prepared, knowing that you’re gonna be stepping into a mine field, there’s gonna be some people that just are gonna take two feet in, they’re gonna go, “You know what? Not my time,” and that’s alright. As long as they’re educated and they understand the process, that’s all I can ever ask for.

BO: Sounds good. Thank you, Dan. We appreciate you spending some time with us. Everybody, you’ve been listening to Structure Talk, a Structure Tech presentation. My name is Bill Oelrich, alongside Tessa Murry and Reuben Saltzman. Thanks for listening. We will catch you next time.