I’ve been ranting and raving about hail-damaged roofs and how messed-up homeowners insurance is for the past couple of blog posts. While digging into this topic with a number of roofing contractors and insurance professionals, I stumbled across some very important information regarding the 15-year mark for roof coverings.

Insurance companies hate them. If you’re planning to purchase a home with a roof that’s more than 15 years old, you might run into some difficulties with your lender and insurance company.

Replacement Cost vs. Actual Cash Value

I touched on this at the end of last week’s blog post, but it’s worth bringing up again. If your homeowner’s insurance covers the Replacement Cost of your roof, this means you could have a dilapidated 21-year-old roof get hit with a hailstorm, and your homeowner’s insurance would cover the full cost of a brand-spankin-new roof.

Here’s a good comparison: you total your 1999 Ford F150, so you go to your auto insurance carrier. They replace your old beater with a 2020 Ford F150. That would be completely insane, right? Well, that’s how it works for roofs if your insurance policy covers replacement costs. That’s why I call this “winning a new roof”.

If your policy covers Actual Cash Value, it means you get a depreciated value settlement if a hailstorm trashes your roof. This makes a heck of a lot more sense to me, but I understand that it could also put some cash-strapped homeowners into a bind.

The 15-year mark

Homeowners insurance companies regularly send out notices to their clients with roofs over 15 years old, switching them from replacement cost to actual cash value for their roof. These same insurance companies will only write actual cash value policies for homes with roofs over 15 years old.

That’s completely understandable, but the problem is that many lenders require a replacement cost insurance policy for the roof, regardless of the age. So what are you supposed to do if you’re buying a home with a roof that’s more than 15 years old and you’re not paying cash for the home? You’ll need to shop around for the right insurance company. They’re out there, but you’ll need to pay a lot more for insurance.

How to determine the age of a roof

As a home inspector, I make no attempt to determine the age of a roof. I’m not aware of any reliable carbon-dating method for roofs either. I’m very good at estimating roof ages, but every once in awhile I’ll be a fair bit off in one direction or the other.

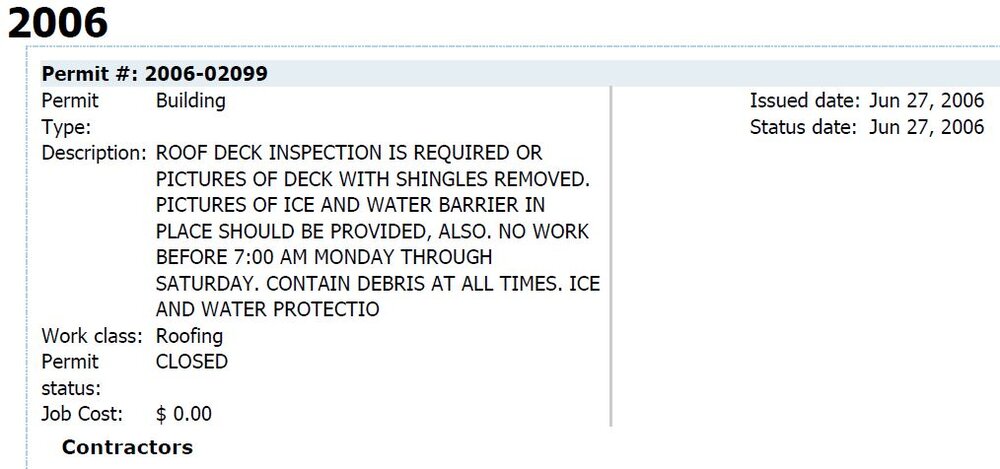

To determine the exact age of a roof at a home you’re buying, it’s helpful to ask sellers for that information. If that’s not possible, check the permit history for the home. As a courtesy to our clients, we order BuildFax reports with all of our home inspections and provide them to our clients. These reports frequently contain the permit history for roof replacements. The screenshot below shows an example of the information provided.

When none of these things are available, we can sometimes find date codes on roof vents, but that’s only a clue. All it really tells us for certain is the age of the roof vent.

To listen to a discussion of all of this, check out yesterday’s podcast with insurance specialist Tim Molgren: